Uber enters its Amazon era

13 years and billions of dollars down the road, the flywheel is starting to spin

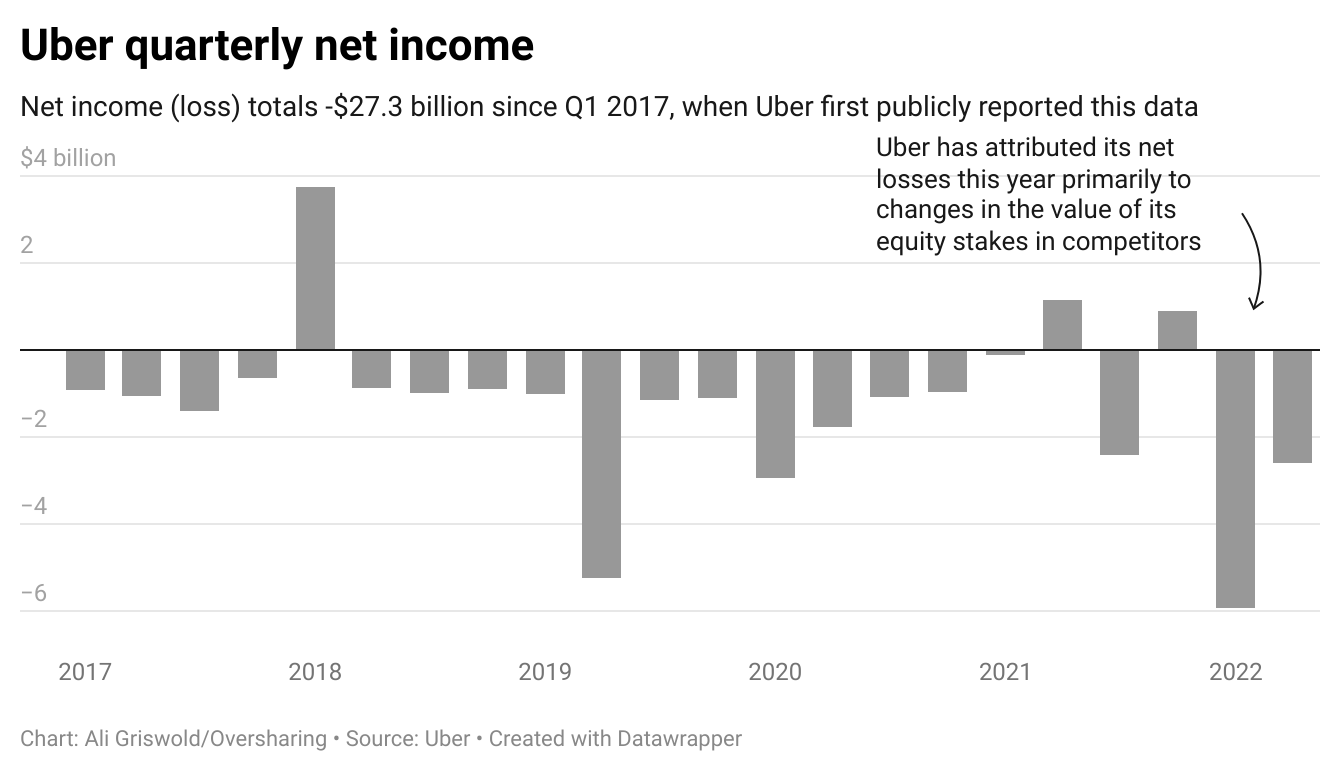

Let’s begin by acknowledging that Uber still loses a lot of money. In the most recent quarter, ended June 30, Uber posted a net loss of $2.6 billion. That brings Uber’s total net income since Q1 2017, the first quarter for which it published financial data, to -$27.3 billion, an absolute value equivalent to the entire market cap of DoorDash.

And yet. Losses aside, the business of Uber is starting to look quite strong.

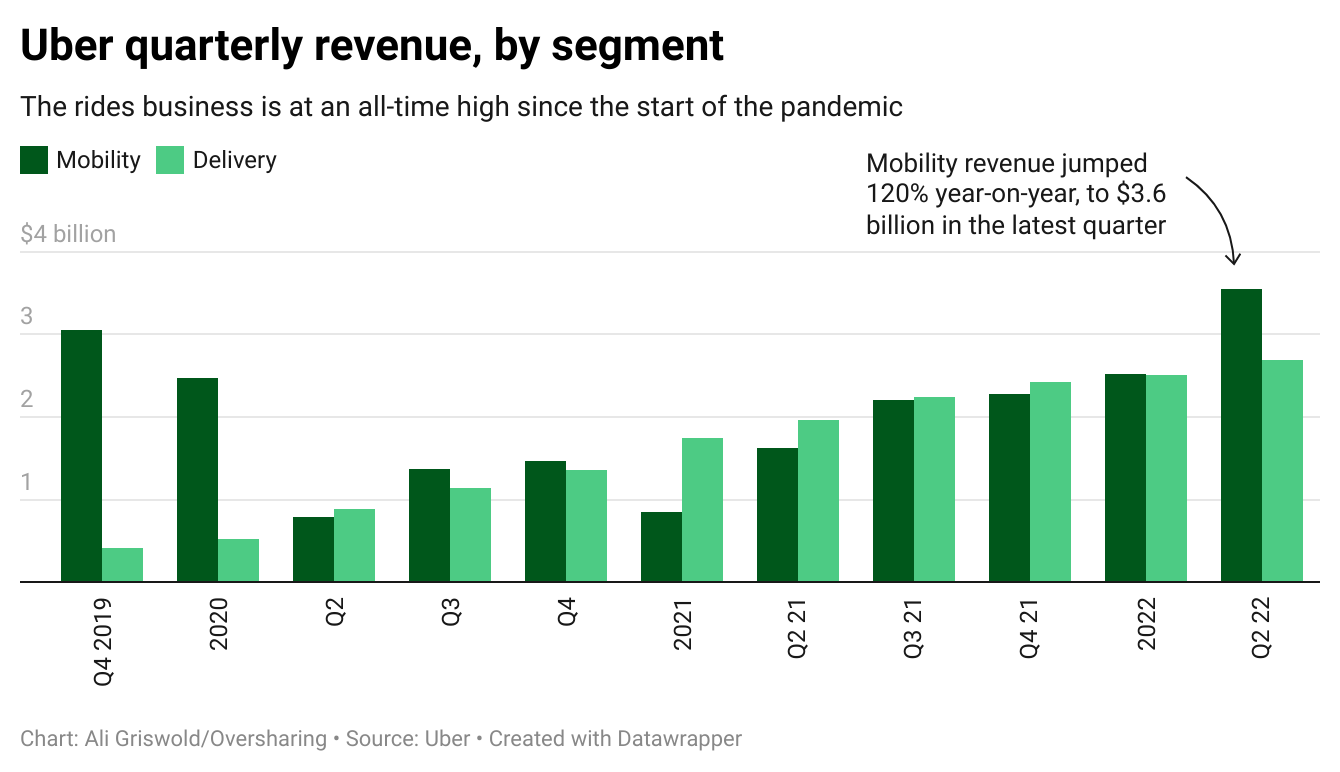

Rides have finally recovered from their covid dip, with $13.4 billion in bookings and $3.6 billion in revenue in the latest quarter, the latter of which jumped 120% over the previous year to an all-time high. Growth in delivery has slowed, as you might expect now that restaurants are back open for dining and people are no longer subject to pandemic lockdowns, but Eats remains a steady revenue generator. In the land of non-GAAP measures, Uber reported adjusted ebitda of $364 million, free cash flow (net cash flows from operating activities minus capex) of $382 million, and positive adjusted ebitda for each of its business segments.

Then there’s the platform. If you believe Uber’s execs, things are getting more efficient. Chief financial officer Nelson Chai said on the investor call that delivery unit economics are better, while CEO Dara Khosrowshahi highlighted improvements to rides pricing and dispatch algorithms that “allows us to improve profitability and/or experience without a tradeoff in terms of top-line growth.” Driver signups, which lagged during the pandemic, were up 76% from the same time last year as more people turn to gig work as a bulwark against inflation and rising costs of living. That was despite a “meaningful reduction in driver supply investments” that Uber said helped to improve its adjusted ebitda margin in rides.

On the customer side, ride wait times in the U.S. are down from 2021, to around 4.5 minutes, and the share of trips that are surged is down too, though whether that means much in a world of dynamic pricing and opaque base rates is for you to decide. Considering how ride-hail has gotten 40% more expensive over the past three years, I’d interpret that more as a sign that Uber’s pricing has stabilized at higher rates where routine surge is less necessary than as evidence of better prices for consumers. These charts from Uber’s investor presentation, btw, are a great addition to the canon of charts without axes. A reminder to send me your favorite axes of evil and to keep fighting the good fight against unlabeled charts and pie charts in all forms.

Finally, there’s Uber One, the membership program Uber introduced late last year and which now counts 10 million members across the seven markets it’s available in. One is Uber’s effort to create its own Amazon Prime, a one-stop member portal that cultivates more loyal, frequent, and higher-spend users. Uber One costs $9.99 a month or $99.99 a year in the U.S. (truly, not $99 or $100) and £5.99 a month or £59.99 a year in the UK, prices that were closer to parity before the pound plummeted. One members get free delivery on eligible Eats orders, more discounts on Uber services, credit if arrival estimates on orders are wrong, and the ability to cancel without fees or penalties. When I opened the Eats app while writing this, a pop-up declared I could save “around £19 every month” with One based on average member savings in the UK, which, lol, seriously overestimates how often I use Uber.

Companies love to compare themselves to Amazon, that pinnacle of late-stage capitalism, for obvious reasons. Startups are also fond of drawing parallels, both to impress investors and to gesture away staggering losses. Amazon is the textbook example of a company that lost money to make money, and loss-making founders love to remind you of that, though they also tend to conveniently forget that Amazon’s losses had nothing on the Ubers of the world and that the Everything Store became reliably profitable after about six years.

Amazon’s cash cow is its cloud-computing division, but its flagship business is Prime, the chimerical membership whose benefits include free next- and same-day delivery, two-hour grocery delivery, access to Prime Video, Music, and the Kindle library, and unlimited photo storage. We know that Prime members are incredibly valuable customers. They spend more than other Amazon users, order more frequently, and renew their subscriptions at exceptionally high rates. (Amazon Day, a more recent addition to the Prime menu, seems designed to curb the shipping costs incurred by particularly voracious Prime users, encouraging them to select a preferred day of the week for delivery so that orders can be batched and sent together.) In his 2016 letter to shareholders, then-CEO Jeff Bezos wrote that he wanted Prime “to be such a good value, you’d be irresponsible not to be a member.”

Ahead of Uber’s 2019 IPO, it ramped up the Amazon rhetoric. Khosrowshahi said in various interviews that Uber aimed to “be the Amazon for transportation” and that “cars are to us what books were to Amazon.” The idea was that Uber’s core ride-hail business would be the portal that brought people into the platform, where they would discover everything else Uber had to offer, like food delivery, bikes and scooters, and, one day, autonomous vehicles. Three years down the line, the scope of that platform is smaller—Uber offloaded its Jump micromobility division to Lime and sold its driverless car unit to Aurora—but the Amazon vision is starting to come into focus.

Ironically, it wasn’t rides but Eats that proved the gateway. Uber’s delivery business surged during covid even as rides cratered, reaching double-digit billions in bookings for the first time ever during the fourth quarter of 2020. On the consumer side, Eats has become a powerful new user generator. In Q4 2020, 56% of first-time delivery customers were new to the Uber platform; in Q4 2021, that share jumped to 60%. Customers who used Uber for both rides and Eats also used the platform more than twice as much, averaging 12.6 transactions per month in Q4 2021 compared to 5 per month for people who only used one Uber service. On the driver side, Eats turns out to be better than rides at bringing workers onto the platform. At the height of the pandemic, transporting food and groceries was widely considered safer than driving around people. Delivery workers are also generally subject to less regulatory oversight than taxi drivers, making them quicker and easier to onboard.

It’s still too soon to say if Uber One has Prime potential, but the early results bode well for Uber. Khosrowshahi told investors on the quarterly call that about 23% of all gross bookings are coming from members and gross bookings per member are about 2.7x that of a regular Uber user, suggesting that the still-small segment of 10 million One members have already formed a super-user base among Uber’s 122 million monthly active platform consumers. The trends with One are a logical extension of what Uber was already seeing in 2020 and 2021—that people who book rides and order food with Uber are higher spend, more frequent consumers.

“It’s really a part of the power of the platform,” Khosrowshahi said. “If you ride with us, if you eat with us, if you drink with us, if you order groceries with us, we just become an everyday part of your life. You top that off with the membership program.”

Yes, Uber still loses a lot of money. No, it’s not Amazon. Yes, it’s still an open question of whether Uber can be profitable, especially without raising prices to the point where it is really only a luxury service. Yes, there’s still plenty to dislike about its labor practices and the steady erosion of workers’ rights through fragmented, precarious gig work. Yes, let’s not forget about delivery fee caps and antitrust and the various other issues that could still, in theory, upend the gig model. All of these things are true. But maybe for the first time, Uber’s proverbial flywheel appears to be spinning on the merits of the platform and not through the sheer force of billions of dollars in venture capital. After 13 years, it’s about time.

Outtakes:

It struck me while listening to Uber’s investor call that everyone on that call—all of the analysts and the Uber execs—were men, and maybe it would be cool if a woman got in the mix, what a radical idea

I had to laugh when Khosrowshahi said Uber “stepped up and designated drivers in the UK as workers, we think it’s the right thing to do.” Last time I checked, Uber was required to reclassify its UK drivers as workers (vs. self employed) after losing its final appeal and long-running legal battle to avoid doing just that at the UK Supreme Court