Everyone is some kind of profitable

No Jokr

Hello and welcome to Oversharing, a newsletter about the proverbial sharing economy. If you’re returning from last time, thanks! If you’re new, nice to have you! (Over)share the love and tell your friends to sign up here.

Oversharing is now a subscriber-supported newsletter. Paid subscribers get three posts per week with the most in-depth analyses of the gig economy, mobility, and urban life; full access to the archive; and exclusive access to comments and community threads. Subscribe now for a special launch period rate of $7/month or $70/year.

Jokr.

Here is a weird TechCrunch interview with Jokr founder and CEO Ralf Wenzel, who claims the year-old ‘instant’ delivery startup is “fully gross profit positive on a group level for our local business across all of our countries after 12 months of operations.”

As a reader, I hoped the follow-up to this statement would be “I’m sorry but what does that mean exactly, what does it mean to be ‘gross profit positive on a group level for our local business across all of our countries’”? Like let’s break that down for a minute, what are the meanings here of ‘group level,’ ‘local business,’ and even ‘gross profit’? It is weirdly sweeping and qualified at the same time, and unlike any profitability metric I’ve heard before, even in the wild west of startup metrics where everyone is some version of profitable. It’s also far too much of a mouthful for anyone to go around saying as though it might possibly be useful. It doesn’t even abbreviate nicely! GPPGLLBAAOC? GPPoaGLfoLBaaooC??

But no, this was not the next question, or if it was that portion of the interview didn’t make the edited transcript. What follows instead is:

TechCrunch: What does this mean now for JOKR’s immediate future?

Wenzel: For us, this is proof point No. 1 that the business model works. This allows us also to grow in a more sustainable way going forward. It makes us become more and more independent of outside capital. With every order that we are delivering, we’re now having a positive contribution margin, and that allows us to basically build the business in a very capital-efficient way going forward.

Wait, so is it GPPGLLBAAOC or is it contribution-margin positive, or are they being used here to mean the same thing? Contribution margin is a term that can be used to mean a lot of different things, as this HBR piece warns, but generally it applies to the unit economics of a service. So in theory if Jokr made money on each delivery, e.g., it took in more revenue on each transaction than it paid out in costs, excluding overhead and other fixed business costs, that would be a positive contribution margin. If true, that would be a big shift for Jokr, which as of last August was reportedly losing a jaw-dropping $159 per order in the U.S. To state the obvious, positive unit economics would be a big improvement from a loss of $159 per delivery!

Such reportedly huge losses have yet to be a problem for Jokr, at least on paper. The company raised $260 million in Series B funding in December at a valuation of $1.26 billion to deliver groceries “before the water boils,” which just goes to show that the unicorn ecosystem is alive and well. “Capital goes where companies are generating the highest efficiency and sustainability,” Wenzel told TechCrunch. “That’s why the whole industry has become more rational.” And sure, if valuing a company of just about a year old with an unproven business model and potentially huge losses at over a billion dollars is your definition of rational, then ok.

More recently, Jokr was said to be in talks to sell its New York business to stem heavy losses, as well as to have quietly exited Europe after about six months of operations, having failed to find a buyer. Business is reportedly better in Latin America, where Jokr told investors it hopes to break even this year. Asked about the possible sale of its New York City operations by TechCrunch, Wenzel said there have been “no strategic shifts” and that “we opened new warehouses and we closed other warehouses,” in keeping with the general equivocal tone of the interview.

Just Eat.

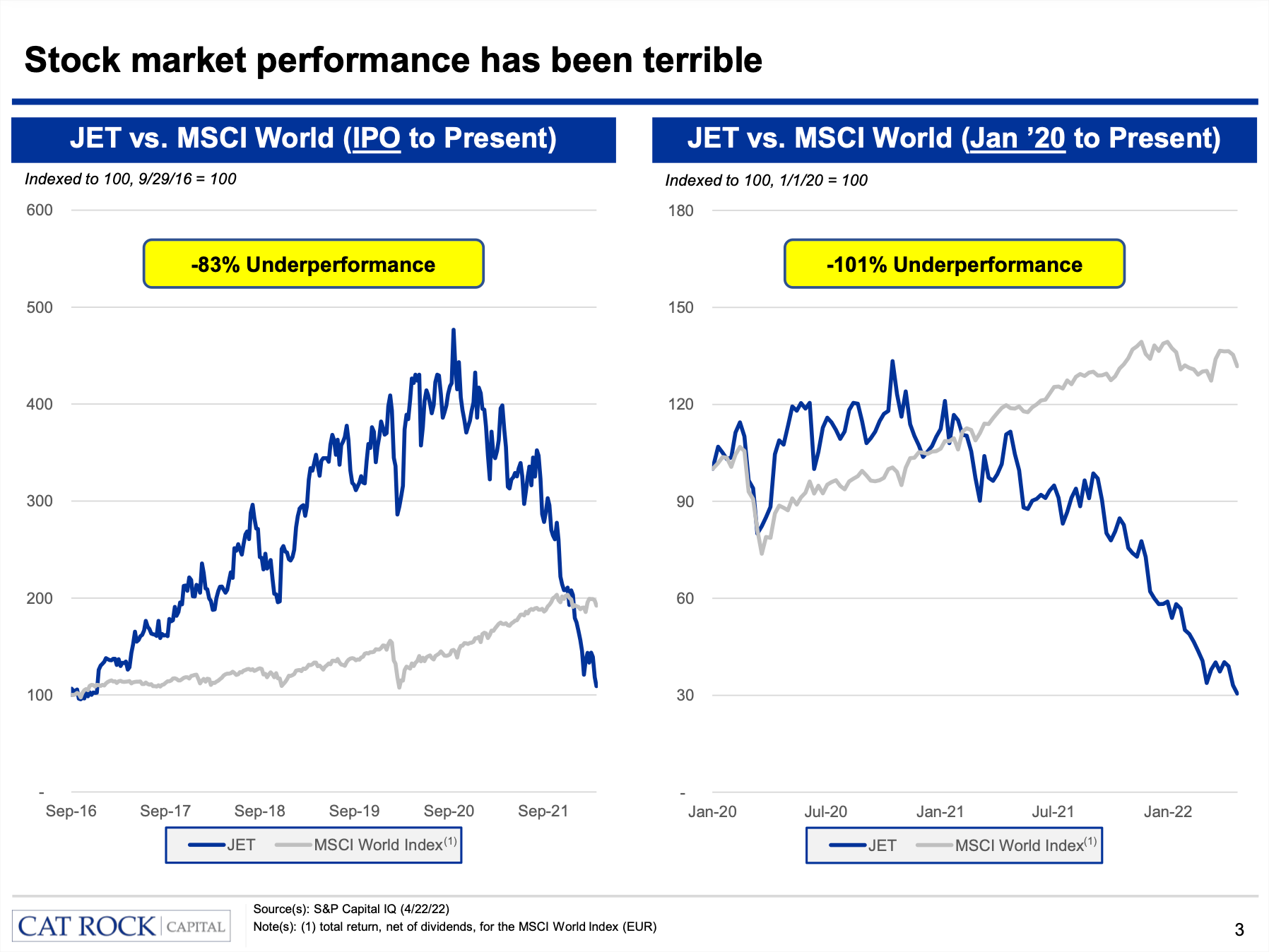

We talked last week about why Just Eat Takeaway soured on Grubhub less than a year after closing its $7.3 billion acquisition of the U.S. firm. One reason seems to be pressure from activist investor Cat Rock Capital, which owns 6.9% of Just Eat and has called for the company to ditch Grubhub and refocus on its core European markets. Cat Rock had already published a 45-page presentation in favor of selling Grubhub on its dedicated website, justeatmustdeliver.com, and yesterday it was back at it with another slide deck, this time urging Just Eat shareholders to vote against reappointing the company’s CFO and Supervisory Board at the May 4 annual meeting.

Cat Rock’s main complaint is that Just Eat’s current management has “overseen a catastrophic destruction of equity value in the past two years,” with the stock collapsing 75% since Just Eat announced its deal to buy Grubhub in June 2020. Cat Rock also alleges that Just Eat led investors to believe that it was in better financial shape than it actually was ahead of the Grubhub deal, only to disclose “that profits had disappeared” shortly after shareholders approved the transaction.

Here is most of that in chart form:

Shareholder votes are due by April 28. Cat Rock invites shareholders with questions or trouble voting to reach out by email, and I like the idea that it is the job of some poor intern to field inquiries from shareholders who are engaged enough to be voting but not tech savvy enough to figure out how.

Cooling off.

Stocks that soared during the pandemic are now cooling as restrictions ease and many people get back to something like normal life:

The onset of Covid-19 changed the way people worked, shopped and dined, helping companies such as videoconferencing star Zoom Video Communications Inc. and at-home workout provider Peloton Interactive Inc. soar. But as restrictions eased and vaccines became widely available, certain consumer behaviors tilted back to prepandemic norms, offering new threats to businesses that thrived in 2020 and 2021.

Investors were especially perturbed by Netflix last week reporting a loss of 200,000 subscribers in the first quarter, its first subscriber drop in more than a decade. Netflix blamed competition, inflation, and the war in Ukraine, with CEO Reed Hastings noting that the pandemic “created a lot of noise” in the business. Netflix forecast it would lose another 2 million subscribers in the spring quarter. The report caused the company’s stock price to plunge and launched a wave of headlines about failure, the end of streaming, and what tech stocks might be next.

Look, obviously investors don’t like it when companies lose money or underperform, but also, what did you expect? There was a global pandemic, life changed massively, people got stuck at home for months on end, and they changed they way they lived and the services they used to cope. Now there is still a global pandemic, but widespread vaccination and eased restrictions have made it more possible to go back to a pre-covid lifestyle, and a lot of people are choosing to do that. That isn’t the fault of any company, it’s just life. It strikes me that this boom-or-bust attitude—the idea that companies must always grow, that it’s not enough to sit in a comfortable middle—is the same one that contributes to unhealthy funding dynamics in Silicon Valley, that slowly throttles the Grubhubs of the world and elevates the Jokrs. Everyone wants to bet on a winner, but what if winning weren’t synonymous with growth?

Other stuff.

Uber, Lyft end mask mandates for riders and drivers. Lyft buys Canadian bikeshare supplier PBSC Urban Solutions for undisclosed price. Deliveroo found guilty of abusing riders’ rights in France. Uber-owned Careem in talks with Saudi authorities to ease ride-hail rules. Lime e-scooters added to Uber app in London and Milton-Keynes. Uber may have to pay $92 million in mass arbitration fees. Brussels letting some Uber drivers go back to work in the capital. Australian startup Splend raises $A150 million to rent cars to ride-hail drivers. Zubale raises $40 million to be temp agency for gig workers. Bird launches bikeshare program in Madrid. Micromobility firm Helbiz lost $72 million on 12.8 million in revenue in 2021. DoorDash releases diversity report. Uber raises fares in Bengaluru by 10%. Woman shot in car while making Uber Eats delivery in Philadelphia. Scottish charity criticized over deal with Deliveroo. Chip-Starved Firms Are Scavenging Silicon From Washing Machines. The False Promise of “Third-Category” Worker Laws. Uber driver dash-cam recording helped FBI catch capitol rioter. Libraries after covid. “Why can we rate Uber drivers but not police officers?”

Superb reporting as always. Somewhere buried in all the news and analyses re mobility/delivery "sharing" is a GUT (Grand Unified Theory) waiting to emerge. If I knew what it was I would tell you, but I think some elements of it are these: a service emerges based on regulatory arbitrage and clever app creation, it is funded to ludicrous heights based on the concept of using capital as a weapon to wipe out the competition, competition emerges in the form of rival startups but also retaliating incumbents (e.g. taxi vs. ridehail, hotels vs. AirBnB), regulators begin to stir and close the arbitrage gap, economics of attackers and incumbents converge, and then a new rival appears: ownership. Why rent the scooter when you can just own it?

Sorry for getting a bit Hegelian there, but there is something in there somewhere. I bet a look at the cycles of taxi de- and re-regulation (pre-ridehail) would prove illuminating.